🌯Inclusive FinTech Knowledge Bites [Week #64]

What’s new in GSMA Mobile Money 2025 report, why inclusion is a go-to-market strategy, and FNB SA’s shift to hybrid access financial hubs.

Hey,

I’m Hugo Pacheco, and this is The Barefoot Economist —a newsletter where, every week, I break down three essential stories on last-mile technology, emerging market innovation, and financial inclusion. Consider it your bite-sized takeaway to stay informed—sharp, insightful, and easy to digest.

This week on The Barefoot Economist:

🤔 GSMA Industry Report on Mobile Money 2025 is out - Whats new?

🔄 From Branches to Business Hubs: FNB's SA shift to hybrid Access

🛒 Inclusion Is Not the End Goal. It's the Go-to-Market Strategy

Enjoy your reading!

1. 🤔 GSMA Industry Report on Mobile Money 2025 is out - Whats new?

Mobile money isn't just a financial inclusion success story anymore — it's now core infrastructure for digital economies across Africa, Asia, and beyond. With 2.1B registered accounts and $1.68T in annual transaction volume, it’s clear: mobile wallets are winning wallets. Sub-Saharan Africa continues to lead, but new growth vectors are emerging in the Asia-Pacific and MENA. The next wave will be defined not by scale but by interoperability, adjacent financial services, and agent network strategy.

🌯 The Barefoot Insight

Growth Is Still Exponential—But Maturing📊 2.1B registered accounts (+14% YoY), with 514M active users monthly.

🏦 $1.68 trillion moved through wallets in 2024. That’s $3.2 million per minute.

Sub-Saharan Africa is still the engine: 1.1B accounts, 66% of global transaction value.

But markets like Cambodia, Vietnam, and MENA are rising fast—helped by proactive regulation.

"It took 18 years to hit 1B accounts. The second billion came in just 5."

Economic Impact is No Longer a Hypothesis📈 Mobile money has added $720B to global GDP by 2023.

In West and East Africa, mobile money contributes 5–8% of GDP.

GDP growth correlation: every +10ppt in mobile money adoption = +0.6–1.0% GDP growth.

This is not just financial inclusion. It's macroeconomic infrastructure.

Unit Economics Are ImprovingARPU (average revenue per user): $3.51, up from $2.86 in 2023.

80% of providers now EBITDA-positive.

But 80% of revenue still comes from customer fees—a concentration risk.

Revenue is growing, but long-term resilience will depend on ecosystem plays (B2B, merchant, credit, insurance).

Transaction Mix is EvolvingTransaction volumes up 20%, values up 16%.

Merchant payments: $105B, growing 21% YoY.

International remittances: $34B, growing fastest at +22%.

Ecosystem transactions (merchant, bill pay, P2P) are outpacing cash-ins and outs.

We're witnessing the quiet exit of cash. But only where agents are strong and digital use cases are sticky.

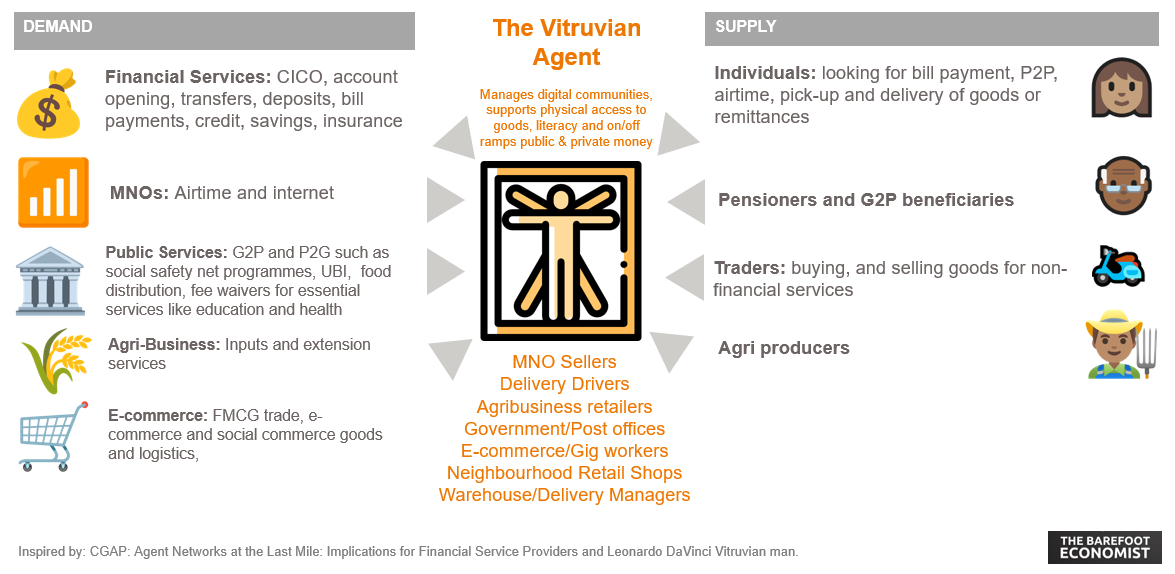

Agent Networks Are Expanding – and Shifting28M registered agents (+20% YoY); 10M active monthly (+17%).

Accessibility doubled since 2021: 755 agents per 100k adults.

Sub-Saharan Africa accounts for 77% of new agent growth.

The agent is still the bridge between the informal and the digital. But the role is shifting: less “cash-in, cash-out” and more last-mile customer education, onboarding, and upselling.

Partnerships boost business models not just a ChannelThe most successful providers (Airtel, MTN, M-PESA) are playing ecosystem chess, not just wallet checkers.

Mastercard + MTN = MoMo cards in 13 markets.

Safaricom + Visa = global payments play.

Temenos, Orabank, PYYPL, PayPal, and others now provide rails, infrastructure, and credibility.

Insight: Partnerships enable scale faster than licensing or building alone. They reduce time-to-market for features like remittances, cards, bill pay, and recurring services — especially in highly regulated environments.

Agent Networks as create a Strategic InfrastructureAgents aren’t a distribution channel; they’re network effects in human form.

Providers that treat agents as sales, KYC, and support channels—not just cash handlers—will win.

Agent density drives not just liquidity but trust.

Providers should tier agents by capability (cross-sell potential, trust level, digital savviness) and deploy services accordingly (e.g., loans via trusted Tier 1 agents).

Playbook shifts = From grow agent count to grow active, trusted, cross-sell-ready agents with tailored incentives.

Where The Next Value LiesFor fintech builders, investors, and regulators, this is the moment to double down. Here are my views on where the next battleground areas are:

Financial services layering (credit, savings, insurance).

Agent segmentation for cost efficiency and growth.

Partnerships for interoperability and last-mile feature delivery.

Mobile money is no longer a product. It’s an operating system for digital economies.

2. 🛒 Inclusion Is Not the End Goal. It's the Go-to-Market Strategy

Most see rural markets as a nice-to-have, but others see their GMV engine.