🌯Inclusive FinTech Knowledge Bites [Week #52]

Financial access unlocked with smart agent segmentation, NuBank & OXXO’s cash strategy for 9M Mexicans, and the future of agency banking in South Africa.

This week on The Barefoot Economist:

💡 Smart Segmentation: Unlocking the Power of New-Age Agents

🏧 NuBank & OXXO: Rethinking Access to Cash for 9 Million Mexicans

📍 No Banking Boundaries: The future of South African agency banking

Enjoy your reading!

Hugo Pacheco, The Barefoot Economist

1. 💡 Smart Segmentation: Unlocking the Power of New-Age Agents

The Business Correspondent Resource Council (BCRC) has proposed to the Insurance Regulatory and Development Authority of India (Irdai) that business correspondents (BCs) be permitted to sell insurance products.

The reimagining of India's BC channel showcases how agent networks can evolve beyond traditional banking services to offer diversified financial products like insurance, thereby increasing their financial viability and impact. With over 500,000 BCs, India's approach demonstrates the potential of leveraging extensive agent networks for greater financial inclusion, even in underserved regions.

🌯 The Barefoot Insight

The Rise of Payment Bank Agents as a Strategic Distribution ChannelNew-age business correspondents (BCs) and fintech agents are evolving beyond cash-in/cash-out (CICO) transactions to higher-value financial services such as wealth management, digital credit, and microinsurance.

The promise of an integrated model: digital lenders who already use BCs to disburse loans have successfully distributed over 3 crore loans worth nearly ₹37,000 crore, proving the effectiveness of this distribution model.

Their ability to sell complex financial products differentiates them from traditional BCs, addressing a key challenge in financial inclusion: expanding product diversity while ensuring last-mile access.

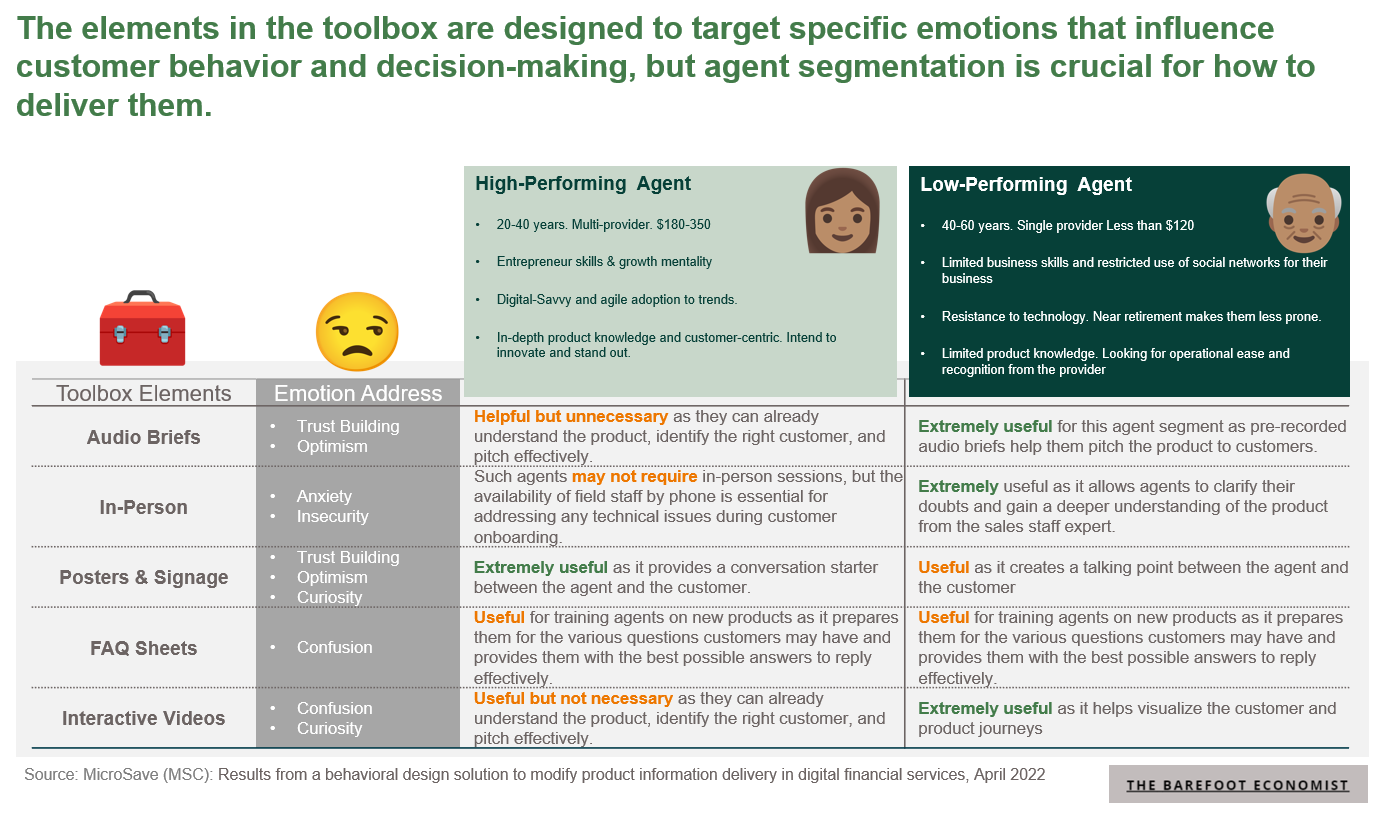

Agent Segmentation is Essential for Scaling Financial ServicesDigital Savviness as a Competitive Edge: Payment bank agents are younger, more agile, and digitally proficient, making them ideal for selling tech-driven financial products.

Mobility Constraints Limit Geographic Expansion: Since most agents operate from fixed retail locations, strategic placement and clustering are necessary to maximise reach.

Trust Deficit in Financial Advisory: While agents are readily available, their lack of financial literacy hinders customer confidence, requiring training and certification programs to improve credibility and a hybrid online-offline communication management toolbox.

Business Model Efficiency: Faster Break-even, Lower CAPEXCompared to traditional BCs, new-age agents achieve break-even within 2-3 months, versus six months to a year for legacy models.

A lower capital expenditure (CAPEX) of $61 vs. $1,065 allows for scalable expansion with minimal upfront investment, making them ideal partners for banks and fintechs looking to deepen outreach.

Agent Retention & Financial Sustainability Require Long-term Value PropositionsHigh agent turnover remains a challenge, but offering sustainable income streams via long-term use cases (e.g., wealth management & digital lending) can reduce churn and enhance financial stability.

Micro and SME credit distribution through BCs unlocks access to underserved businesses, aligning agent incentives with broader economic growth.

What are the next Priority Use Cases?Wealth Management: Expanding agent offerings beyond daily transactions can create stickiness and higher margins.

Digital Credit: Seamless credit distribution via embedded finance solutions (e.g., BNPL, SME loans) could redefine financial inclusion.

Insurance Aggregation (Adjacent Opportunity): Climate risk and health microinsurance can be distributed through BCs, addressing underserved populations while diversifying agent revenue streams.

Final Thought: What Can African Markets Learn?The segmentation and specialization of agent networks in India highlight a blueprint for Africa’s fintech and banking ecosystems. By leveraging digitally proficient BCs, offering commission-based higher-value products, and adopting low-CAPEX models, African agent networks can enhance financial inclusion while building sustainable agent-driven economies.

💡 Access The Agent Network OS and unlock unique frameworks, webinars and business model samples that will help you understand how to scale and optimise your agent networks using technology insights, partnership design and do-it-yourself templates.