🌯Inclusive FinTech Knowledge Bites [Week #73]

Ethiopia’s agent gap reveals key challenges in inclusive finance. Offline transactions: from USSD to sync queues, and PAPSSCARD’s role in unifying African payments.

Hey,

I'm Hugo Pacheco, and this is The Barefoot Economist, your weekly field guide to last-mile tech, fintech inclusion GTM, and innovation in emerging markets. Every edition delivers 3 sharp, no-fluff takeaways built for people solving real problems in cash-heavy, trust-first economies.

This week on The Barefoot Economist:

🔌 What Ethiopia’s Agent Problem Tells Us About Inclusive Finance

📟 USSD to Sync Queues: The Real Infrastructure of Inclusion

💳 PAPSSCARD: Disruption or Unification in African Payments?

Enjoy your reading!

🔌 Disconnected at the Edges: What Ethiopia’s Agent Problem Tells Us About Inclusive Finance

Telebirr is everywhere but cash-in, cash-out still feels out of reach. Here’s why agents matter more than ever.

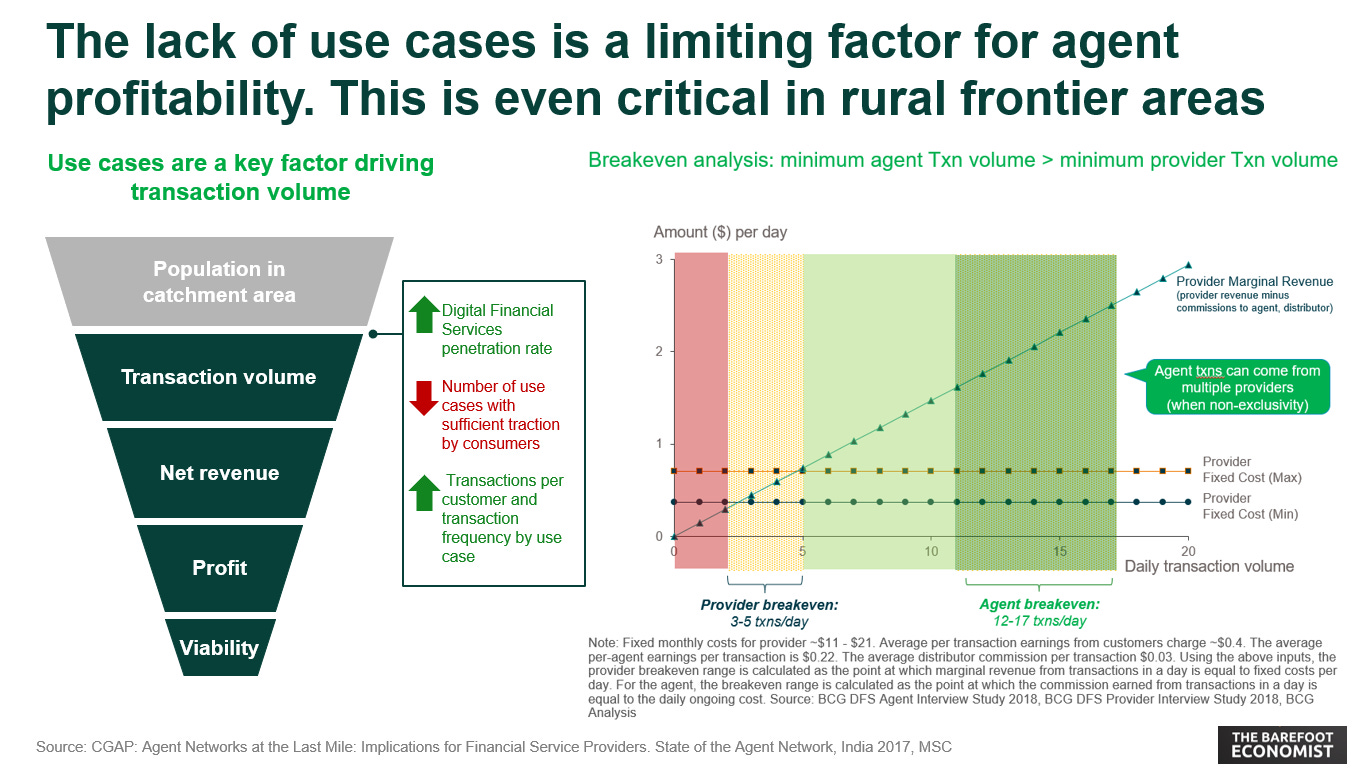

Ethiopia’s mobile money story is rocketing in account growth but limping on agent activity. Platforms like Telebirr have added millions of accounts, yet the average agent handles less than one transaction per day. Unlike Kenya’s agent-led model, Ethiopia’s digital finance push is bypassing the boots-on-the-ground. Because the business case for agents is weak, the digital journey is too DIY, and the timing missed the “trust moment” when agents could have mattered most. Now, Ethiopia is trying to retrofit a digital-first model into a cash-first reality, without the glue of functioning agents to hold it all together.

🌯 The Barefoot Insight

Growth ≠ UsageEthiopia saw a 1,238% increase in mobile money accounts and a 1,726% rise in agents (2019–2024), yet agent activity remains dismal. An average of 314 transactions per agent per year signals systemic inactivity. This isn’t scale, it’s surface.

Digital-First, But Human-LastSelf-registration, utility payments integration, and centralised services make agents increasingly irrelevant. But for 54% of Ethiopians without bank accounts (World Bank Findex 2022), CICO agents are still critical, if they actually function.

The Kenyan Comparison Doesn’t FitKenya’s agent model worked because:

Banking was exclusionary and hard to access.

M-Pesa arrived when cash digitisation was urgent.

Agents were essential, not optional.

Ethiopia introduced mobile money post-digital adoption. It skipped the messy middle, where agents build trust, teach usage, and move cash.

Agents Are Bad Business (Right Now)A Telebirr agent earns more selling airtime than doing CICO. The commission structure punishes effort and liquidity risk: 5% on airtime, but only a fraction of that on money transfers. Why serve customers when scratch cards pay better?

Beyond this, liquidity kills agent viability as agents face major cash flow and rebalancing constraints. With poor access to cash points and no predictive demand tools, they’re flying blind. Unsurprisingly, most opt out or hang a sign and do nothing.

Rethink the Agent, Don’t Just Replace ThemEthiopia’s mobile money ecosystem isn’t broken, it’s unfinished. But it cannot succeed on digital rails alone. A payments platform without a trust network (read: reliable agents) is just a wallet with fewer ways to fill or empty it.

To fix this:

Redefine agent roles beyond CICO and think: customer education, onboarding, and digital ID assistance.

Adapt KYC and KYA policies to support informal entrepreneurs and thin-file actors as viable agents (especially women).

Improve liquidity models through agent float sharing, digital escrow, or last-mile rebalancing partnerships with non-competitive industries.

Rebuild the business case with tiered commissions and use-case-based incentives.

If the agent model doesn’t fit as imported, maybe it’s time to design one fit for Ethiopia’s hybrid economy, where trust in cash still rules, but digital rails are quietly increasing over the market.

Like this framework?

Subscribe to get one like it every week.

📟 From USSD to Sync Queues: The Real Infrastructure of Inclusion

Where low bars meet high impact and disconnection is a feature, not a bug.

Digital finance in Africa doesn’t happen because of connectivity; it happens despite it. In towns where 3G comes and goes like rainclouds, fintech survives thanks to USSD menus, SMS logic flows, and agent apps that think like WhatsApp in aeroplane mode: store now, sync later. This isn’t “nice-to-have”. It’s essential design for a continent where 47% of the population is still offline, and data eats up to 9% of monthly income.

The best offline-first fintechs don’t wait for permission from the cloud. They build for drops, cache intelligently, sync securely, and architect locally, all while staying compliant and keeping fraud in check without real-time scoring. This isn’t about lower-tier tech. It’s about higher-res thinking.

🌯 The Barefoot Insight

Build for Disconnection, Not for DowntimeTruth: Most fintechs build like they’re in San Francisco. Africa needs code that assumes the lights will flicker and still works. What does it mean?

Cache every action locally. SQLite, Room, Hive, pick your weapon.

Sync asynchronously. Think WhatsApp queue logic + transaction-level security.

Communicate clearly: show users when things are pending, syncing, or done.

If your fintech can’t function with zero bars and no Wi-Fi, it’s not inclusive. It’s broken.

USSD is the Backbone. Treat it with Respect.Truth: USSD isn’t legacy tech. It’s foundational infrastructure for financial inclusion. Why does it matter?

950M+ Africans are mobile subscribers. Most are still on feature phones.

USSD doesn’t need apps, data, or even literacy in some cases.

Design with timeouts (3 min), PIN logic, and session fallbacks in mind.

Good Example: Moniepoint (*5573#) processes millions in rural Nigeria. Clean, reliable, no internet needed.

SMS ≠ Notification. It’s a Transaction Channel.Truth: SMS is your Plan B and sometimes your Plan A. Use cases?

Loan repayments: "REPAY 1000"

Approvals: "Reply 1 to accept"

Alerts + Two-Way Chat for support or KYC.

Tools like Africa’s Talking and FrontlineSMS let you automate this cheaply and at scale.

Queues & Caching: The Offline HeartbeatTruth: If your POS or agent app doesn’t queue transactions locally, it’s already failing users. What’s required?

Device storage that holds encrypted payloads until connection resumes

Metadata tagging: user ID, timestamp, geo-coordinates

Sync logic that handles dedupes, retries, and eventual consistency

This is what separates serious platforms from pilotware.

Infra Must Touch Grass. Cloud Isn’t Always King.Truth: Cloud latency kills UX in the bush. But full-on-prem breaks budgets.

Smart play?

Hybrid infrastructure: core logic local, analytics/cloud ops remote

Partner with local providers (MainOne, Safaricom Enterprise) to reduce latency

Event-driven backends (Kafka, NATS, Debezium) to handle sync storms

Think low latency + auditability + survivability. Not just scalability.

Secure What You Can’t SeeTruth: Offline = blind spots. Your app needs to catch fraud before it’s connected. Which tactics can we use?

Device-level encryption (AES-256)

JWT-based digital signatures

Auto-locks on GPS anomalies or sync skips

Tiered limits and transaction caps offline

Trust is built offline and confirmed online. Don’t wait for the backend to shout "fraud".

Compliance Doesn’t Pause When the Signal DropsTruth: KYC, AML, and audit trails need to happen even when the backend is offline. What are the real-world practices?

Tiered KYC: SIM-level OK for low-value; documents for full access (sync later)

Tamper-proof logs: UUIDs, Merkle trees, append-only ledgers

Store raw data locally, encrypt with region-bound keys, sync for compliance reports

Auditors don’t care if you were offline. Regulators even less.

Tool Stack Matters. Choose Like a SurvivalistTruth: Not all tech plays well with weak connections.

On-device:

Android: Room, WorkManager

Flutter: Hive, Drift

Web: IndexedDB, PouchDB

Backend:

Firebase/Supabase = fast prototype, not fintech-grade

Hasura + Postgres = control + offline syncing

Kafka + Redis = handle real-time sync storms without meltdown

Offline-first isn’t a constraint. It’s a design advantage if done right. African fintech isn’t waiting for 5G. It’s thriving on caching queues, GSM pipes, and agents who know your name.

Want to serve the real Africa? Building like the internet is optional.

Because most days, it is.

Get weekly takeaways like this in your inbox

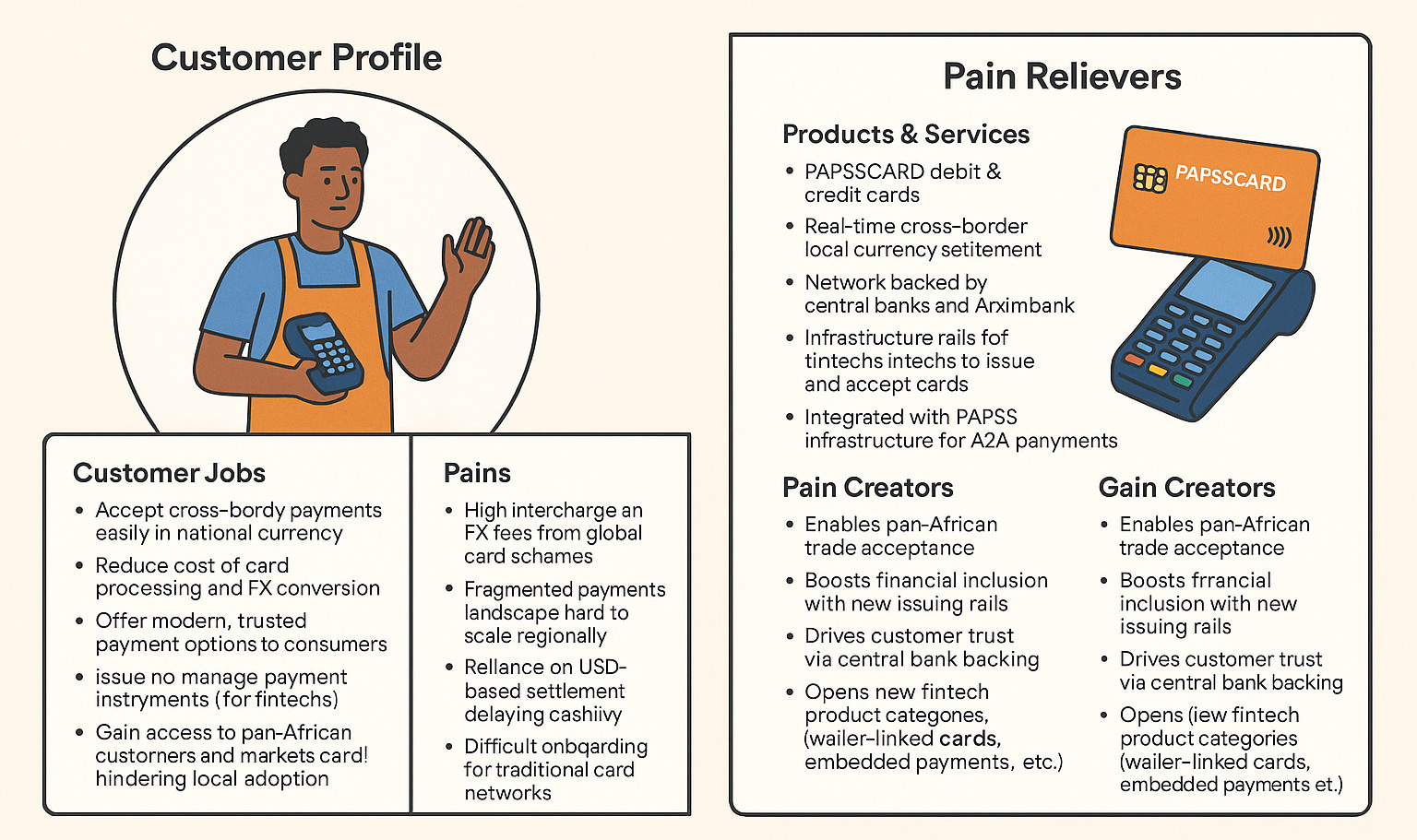

💳 PAPSS CARD: Disruption or Unification in African Payments?

For a continent that leapfrogged card rails in favour of mobile wallets, USSD menus, and Account-to-Account (A2A) payments, the launch of a pan-African card scheme sounds like a plot twist. But it's not a regression, it's a recalibration.

On June 27, Afreximbank, PAPSS, and Mercury Payment Services launched PAPSSCARD, an interoperable debit and credit card network spanning 16 African countries, aiming to anchor trade within Africa, reduce FX leakage, and cut reliance on Visa/Mastercard infrastructure.

“It empowers us to move money swiftly, securely, and affordably across our borders,” said Afreximbank President Benedict Oramah.

This is not just a card. It’s a sovereignty play, a retail strategy, and a regional integration lever all in one.

🌯 The Barefoot Insight

PAPSSCARD isn’t trying to reverse the mobile money revolution; it’s building a layer on top of it. This is about expanding the payment toolkit in a way that works within African systems, not around them. And while the move may look traditional on the surface, underneath it’s a bid to unify fragmented payments ecosystems under an African standard.

Will it disrupt Visa and Mastercard’s dominance? Maybe not tomorrow. But it changes the power dynamics. And in infrastructure, that’s the first step toward sovereignty.

Here are my key takeaways.

From Sovereignty to StrategyAfrica has been paying a hidden tax, interchange fees, FX spread, and data extraction, by relying on global card schemes. PAPSSCARD offers a continental alternative aimed at preserving value within Africa. This echoes Europe’s moves to reclaim payment sovereignty via the European Payments Initiative.

It's Not the Card, It's the RailsThis isn’t a plastic-first future. It’s about building shared infrastructure that supports multi-rail payments: QR, virtual cards, and digital wallets. The card form factor is just one access point. The real power is interoperability via local currency settlement, backed by central banks and PAPSS.

Merchants May HesitateCard acceptance habits are deeply ingrained legacy = trust. Shifting away from Visa/Mastercard rails will require merchant incentives, customer trust-building, and deep integrations with local fintechs and acquirers. Without this, adoption stalls.

Currency Conversion = the Killer Feature.The ability to spend in one’s national currency across 16 countries without conversion or dollar settlement is a game-changer. If PAPSSCARD can crack this at scale, it’ll become a sticky solution for SMEs, freelancers, and digital entrepreneurs.

A Green Light for African Fintech IssuersThis opens the door for local fintechs to issue cards under African terms. Expect a wave of PAPSSCARD-compatible wallets, embedded finance use cases, and cross-border SME tools. It’s a platform moment for innovators.

See you next week!

Hugo Pacheco